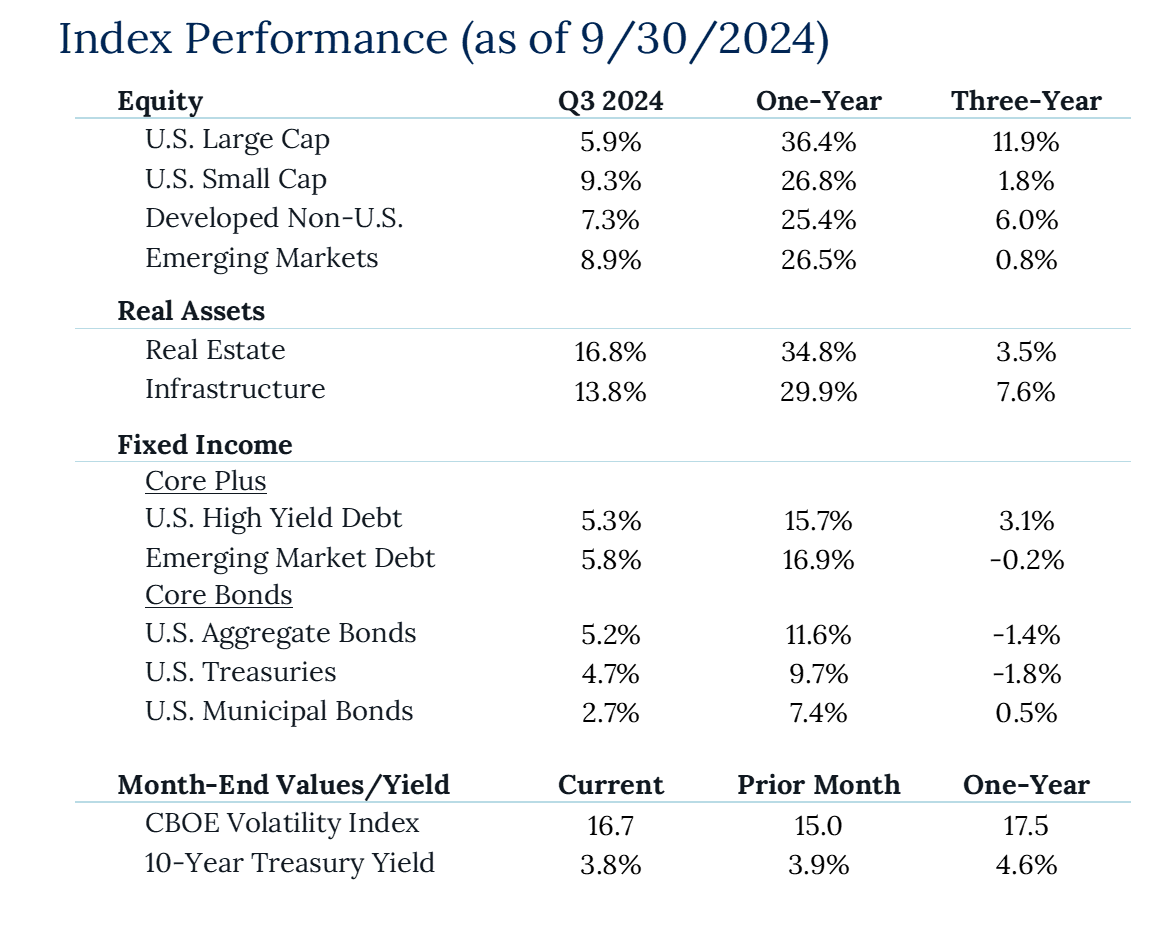

Markets surged in Q3, fueled by the first rate cut of the cycle. This pivotal shift sparked a remarkable rotation, with previously overlooked assets stealing the spotlight. REITs, small caps, value stocks, and international markets outperformed. The weakening US Dollar propelled international markets and expansionary monetary and fiscal policy measures sent Chinese equities soaring over 20% for the quarter. Gold shone brightly as well, reaching new highs, though oil sold off on weakening demand. Bond performance was back in a big way as yields dipped and the once written off “60/40” portfolio is up double digits in 2024. The US economy is on solid footing after enduring years of high inflation and appears to be on track to achieve the Fed’s coveted soft landing scenario as inflation has cooled but economic growth has remained on trend.

Key Takeaways

- Market Rotation: The first rate cut of the cycle boosted markets and sparked a significant rotation. Interest-rate sensitive and previously overlooked assets gained favor, with small caps, international markets, and value stocks outperforming. REITs and infrastructure saw substantial gains, while longer-term bonds outpaced short-term bonds.

- International Equities: Lower rates and a weakening US Dollar led to impressive gains in international markets for Q3. Developed markets showed strong performance as European and Japanese equities were up +6.6% and +5.7%. Small caps were the standout performers, posting a remarkable 10.7% gain. Emerging markets also thrived, with Chinese equities soaring 23.5% due to expansionary monetary and fiscal policy measures

- Commodities: Gold reached new highs in Q3, climbing 13% for the quarter and an impressive 42% over the past year. Oil and natural gas prices, however, declined by 12% and 10% respectively, leading to lower consumer energy costs but potentially signaling weakening demand, especially in China.

- Bond Market Revival: The lower yield environment in Q3 breathed new life into bond markets. Emerging Market debt, High Yield, Investment Grade Corporates, and Treasuries, all posted gains exceeding 5% for the quarter. Over the past year, these sectors have delivered double-digit returns, marking a significant turnaround in fixed income performance.