Market volatility overshadowed stellar economic growth figures for Q3, as real GDP continues to be above trend. Job growth slowed, but weekly jobless claims hit a five-month low, suggesting the payroll data may not fully reflect the underlying strength of the labor market. Commodity markets reflected global economic uncertainty, with gold and oil prices rising. Meanwhile, China’s economic growth slowed, prompting the government to announce stimulus measures. Market performance was broadly negative, with yields rising substantially as investors question whether the Fed will need to slow down the pace of rate cuts.

Key Takeaways

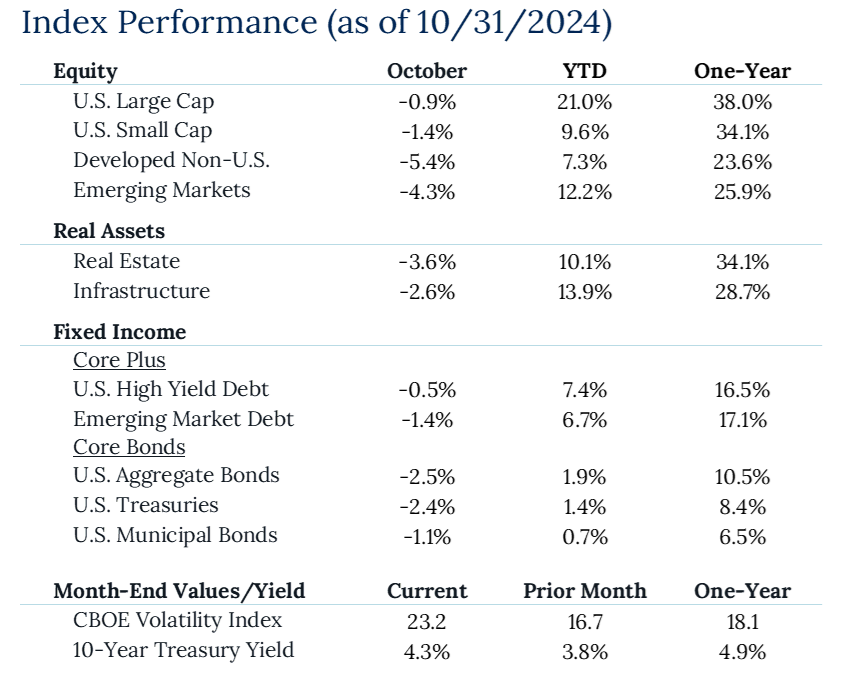

- Market News: The October economic landscape was characterized by rising market volatility. Resilient economic activity (+2.8% QoQ annualized) following the Fed’s initial outsized rate cut has market participants questioning whether the Fed will need to slow its pace. Treasury yields climbed to their highest since midJuly, which triggered a sell-off across stocks and bonds.

- Labor Market: October’s job growth slowed to just 12,000 new payrolls. This report was heavily impacted by hurricanes and the Boeing strike. However, weekly jobless claims hit a five-month low, which could signal that payroll growth was more reasonable than indicated.

- Global Tensions: Commodity markets reflected global economic uncertainty, with gold reaching fresh highs and up 30% year-to-date. Oil rose 3% in October after a volatile period of ebbs and flows related to the conflict in the Middle East. The U.S. dollar jumped versus other currencies in October which weighed heavily on Non-U.S. equity results for the month.

- China: Economic challenges continued for China, with Q3 growth expanding at 4.6%, below the government’s 5% target. The slowdown, driven by sluggish consumption and a property sector slump, prompted Beijing to announce significant monetary and fiscal stimulus. Chinese equity markets rallied on the initial announcement, however, equity markets gave up their momentum, ending down over 6% in October.